A LASTING LEGACY:

GUIDE TO INHERITANCE

AND ESTATE PLANNING IN IRELAND

Our 2025 guide to inheritance and estate planning contains the essential information you need to consider as part of a successful and impactful inheritance plan.

The key considerations are summarised in this interactive article and the full guide is available to download as a pdf using the form below.

01

Introduction –

Catriona Coady

Inheritance planning is one of the most important steps you can take to support and protect your loved ones.

Introduction

Protecting your wealth. Creating your legacy.

We are in the midst of the ‘Great Wealth Transfer’ – baby boomers – those aged between 61 to 79 have accumulated valuable assets such as property, pensions and shares. And as a result, now more than ever, they (together with the builders – those aged over 80) want to protect what that have earned through seamless intergenerational transfer. With this comes a requirement for financial and inheritance planning along with many other matters to consider in building a lasting legacy.

This guide aims to address the planning issues to manage the transfer of wealth to the next generation, from financial planning to gift and inheritance tax in Ireland, but it also outlines the significance of business succession, family governance and the changing nature of families in an inheritance plan. So, while financial planning and tax are important factors in any transfer of wealth, this guide seeks to address best practice and legal issues to consider as part of a successful and impactful succession plan.

The overriding message from this guide is to start planning at an early stage and before it gets too late when plans can be rushed and not as effective as they could be.

Get in touch today to learn how we can support you in planning for the future.

CATRIONA COADY

Head of Tax, Goodbody

Introduction

Protecting your wealth. Creating your legacy.

CATRIONA COADY

Head of Tax, Goodbody

We are in the midst of the ‘Great Wealth Transfer’ – baby boomers – those aged between 61 to 79 have accumulated valuable assets such as property, pensions and shares. And as a result, now more than ever, they (together with the builders – those aged over 80) want to protect what that have earned through seamless intergenerational transfer. With this comes a requirement for financial and inheritance planning along with many other matters to consider in building a lasting legacy.

This guide aims to address the planning issues to manage the transfer of wealth to the next generation, from financial planning to gift and inheritance tax in Ireland, but it also outlines the significance of business succession, family governance and the changing nature of families in an inheritance plan. So, while financial planning and tax are important factors in any transfer of wealth, this guide seeks to address best practice and legal issues to consider as part of a successful and impactful succession plan.

The overriding message from this guide is to start planning at an early stage and before it gets too late when plans can be rushed and not as effective as they could be.

Get in touch today to learn how we can support you in planning for the future.

02

What is

Inheritance Tax?

Understanding taxation is the starting point for gift and inheritance planning.

What is Inheritance Tax?

While tax should not be the sole consideration, understanding tax is an important point for gift and inheritance planning. Capital Acquisitions Tax (CAT) is the tax that is levied on gifts and/or inheritances.

Capital Acquisitions Tax is payable by the beneficiary of a gift or inheritance once they exceed the relevant tax-free CAT group threshold.

The current Capital Acquisitions Tax rate is: 33%

Capital Acquisitions Tax applies when the aggregate amount of all gifts and inheritances exceeds a certain threshold for the applicable Group.

|

Relationship to giver |

Threshold

|

|---|---|

|

Group A A child of the person giving the gift or inheritance. Child includes an adopted child, stepchild, child of a civil partner and certain foster children.* |

€400,000 |

|

Group B A parent, brother, sister, niece, nephew, grandparent, grandchild, child of the civil partner of a brother or sister, lineal ancestor or a lineal descendant of the person giving the gift or inheritance. |

€40,000 |

|

Group C People with a relationship to the disponer not already covered in Groups A or B |

€20,000 |

|

Relationship to giver Group A A child of the person giving the gift or inheritance. Child includes an adopted child, stepchild, child of a civil partner and certain foster children.* |

|---|

|

Threshold

€400,000 |

|

Relationship to giver Group B A parent, brother, sister, niece, nephew, grandparent, grandchild, child of the civil partner of a brother or sister, lineal ancestor or a lineal descendant of the person giving the gift or inheritance. |

|

Threshold

€40,000 |

|

Relationship to giver Group C People with a relationship to the disponer not already covered in Groups A or B |

|

Threshold

€20,000 |

03

Key Exemptions

and Reliefs

There are a number of important exemptions and reliefs to be aware of

Key Exemptions and Reliefs

In addition to the group thresholds, there are a number of important exemptions and reliefs to be aware of that can apply to either reduce the amount of Capital Acquisitions Tax due on a gift or inheritance.

The table below highlights some of the exemptions and reliefs you may be eligible for. However, specific conditions may apply to each exemption or relief. We recommend consulting the guide for full details.

Spouses/Civil Partners Exemption

Inheritances taken between spouses/civil partners are exempt from CAT and are ignored for aggregation

This exemption does not apply to cohabitants.

Small Gift Exemption

A beneficiary can receive up to €3,000 from any other person in a calendar year without having to pay CAT.

This allows for the easy and incremental transfer of wealth and can make a difference if applied early.

Support, Maintenance & Education Payments

Payments made to a beneficiary, up to age 25, for support, maintenance or education can be exempt from CAT.

Dwelling House Exemption

A gift or inheritance of a dwelling house can be received free of CAT.

Qualifying Expenses of Incapacitated Persons

If for a medical reason a beneficiary is incapacitated and receives a gift or inheritance to support with qualifying medical expenses an exemption from CAT is available.

Section 73

Provides an option of paying a beneficiary’s CAT bill on a gift without the payment itself being considered a further taxable gift.

Section 72

A Section 72 life insurance plan is a policy to cover the inheritance tax bill of a beneficiary. It allows a beneficiary to inherit assets without then having to find the money to pay a significant tax liability.

04

The importance

of Valuation Dates

Being aware of these dates can greatly help when formulating inheritance plans.

THE IMPORTANCE OF DATES

The date of a gift is generally the date it is received and the date of an inheritance is usually the date of death of the person leaving the inheritance.

The valuation date determines the date by which a CAT return must be filed, and the tax must be paid.

Effective planning is essential to ensure beneficiaries have enough time to meet tax payments, especially when the valuation date falls between January 1 and August 31.

Valuation Dates |

Pay and File Dates |

|---|---|

1 January to 31 August |

31 October of the same year/extended ROS deadline |

1 September to 31 December |

31 October of the following year/extended ROS deadline |

05

The value

of making a plan

From a financial planning perspective, a simple first step is pulling together a list of assets and liabilities

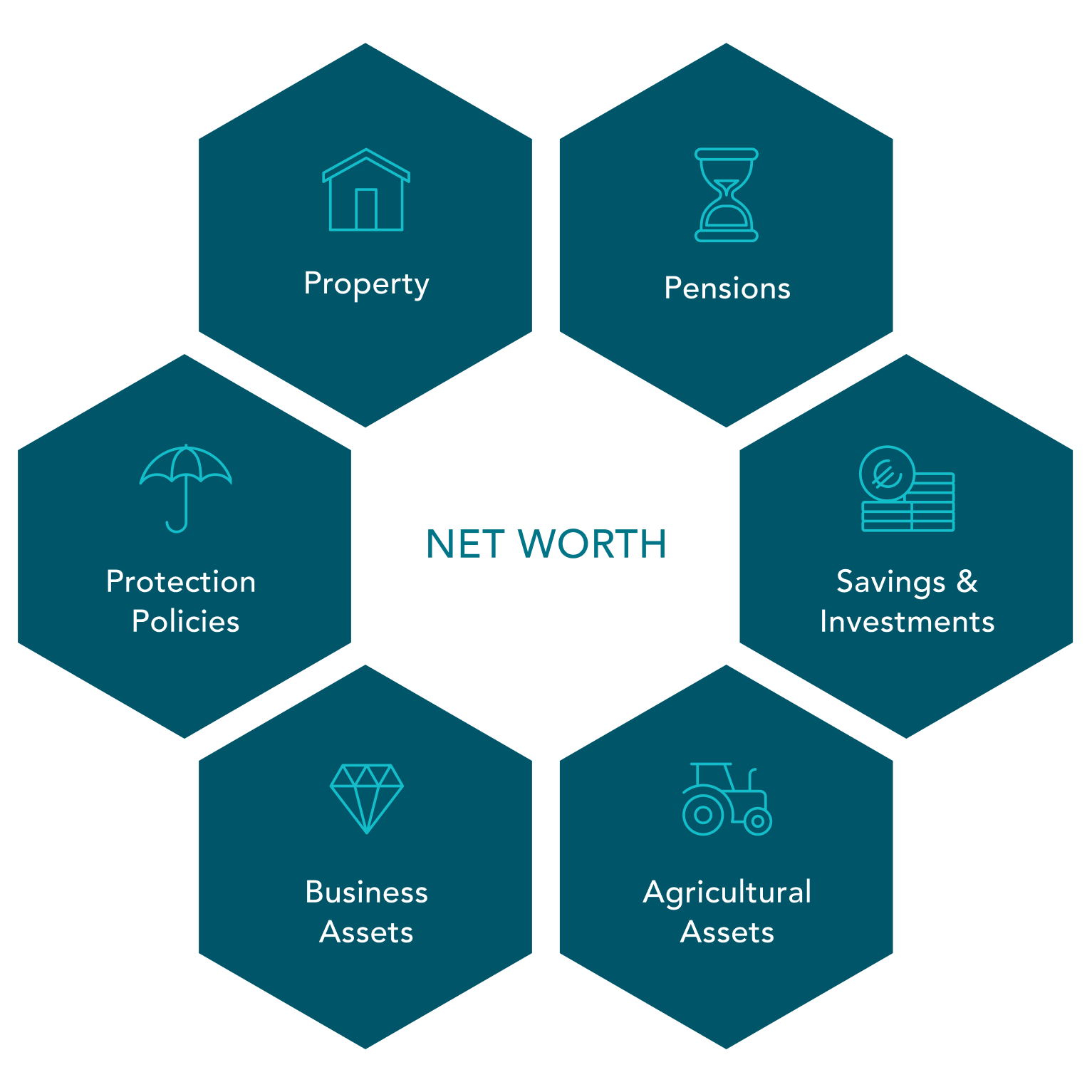

THE VALUE OF MAKING A PLAN

Those who wish to plan for their estate and inheritance often don’t know where to start; they may be thinking about it but can find the conversation difficult. However, in our experience a review of all assets be they property and financial is a good place to start building a plan for the transfer of these assets. From a financial planning perspective, this is as simple as pulling together a list of assets and liabilities or “net worth”.

The 4 ‘Ps’ are key considerations when making an inheritance tax plan.

Property

Property is a major part of personal wealth in Ireland. Understanding your options can help protect it and minimize tax liabilities on future sales.

Protection

Life insurance, mortgage protection, and death-in-service benefits are often overlooked. Sometimes these polices exceed the value of the assets they cover. Ignoring these can lead to underestimating your long-term net worth.

Pensions

Pensions often make up a considerable part of an estate. They not only provide income in retirement but can also provide benefits to other people in certain circumstances such as in the event of death.

Portfolios

Investment portfolios can play an important role in growing, preserving and passing on wealth. Deciding how to transfer shares and other investment securities is an important part of any inheritance plan.

06

Structured

Giving

There are a number of ways you can provide to children or grandchildren in a structured way.

Structured Giving

There are a number of ways you can gift to children or grandchildren in a structured way. We recommend consulting the guide for full details.

Savings Fund Bare Trusts for minor children

|

Involves parents gifting the value of the current CAT threshold or a portion of it to a child under 18. No CAT arises on this gift assuming that the threshold has not previously been utilised and that the threshold is not exceeded. |

|---|---|

Family Partnerships Limited and Unlimited

|

Where there is a concern about children having access to funds at age 18 and provided that there are sufficient funds or assets to warrant it, a family partnership can be formed to hold assets. This allows beneficial ownership of assets to pass to others (usually children) without control being passed.

Such partnerships are generally limited or unlimited. |

Trusts |

Trusts are a useful means of providing control or protection around a gift or ultimately an inheritance. Types of trust include:

|

|

Savings Fund Bare Trusts for minor children

|

|---|

|

Involves parents gifting the value of the current CAT threshold or a portion of it to a child under 18. No CAT arises on this gift assuming that the threshold has not previously been utilised and that the threshold is not exceeded. |

|

Family Partnerships Limited and Unlimited

|

|

Where there is a concern about children having access to funds at age 18 and provided that there are sufficient funds or assets to warrant it, a family partnership can be formed to hold assets. This allows beneficial ownership of assets to pass to others (usually children) without control being passed.

Such partnerships are generally limited or unlimited. |

|

Trusts |

|

Trusts are a useful means of providing control or protection around a gift or ultimately an inheritance. Types of trust include:

|

07

The Importance

of Making a Will

One of the main reasons for making a will is that it provides a set of instructions for the transfer

The Importance of Making a Will

A vital point to note:

One of the main reasons for making a will is that it provides a clear set of instructions for the transfer of property by means of a legal document.

Under the rules of intestacy, if this is not done the property is left to the State to divide the assets of the deceased.

As life circumstances change, existing wills should be updated in accordance with current circumstances and regardless of changing circumstances should be revisited every 3 to 5 years to be updated if necessary.

A will is valid once it:

-

It is made in writing.

-

The testator is over 18 years old.

-

The testator has capacity to make a will.

-

The testator signs or marks the will, at the end of the document, and acknowledges it in the presence of two witnesses.

-

The testator’s two witnesses also sign the will in the presence of the testator.

-

Neither of the testator’s witnesses – or their spouses or civil partners – receive anything in the will. Gifts to them will not be effective.

Enduring Power of Attorney (EPA)

An EPA is sometimes made at the same time as making a will and it is a legal document that can be set up by a person (a donor) to allow another person (an attorney), to look after their financial or personal affairs.

A donor can give the attorney the power to make decisions regarding their property and affairs, including the power to:

-

Sell, exchange, mortgage or gift your property (subject to some limitations)

-

Buy property on behalf of the donor

-

Carry on a trade or profession on the donor’s behalf, where it is lawful to do so

-

Carry out any contract the donor was a party to

-

Pay debts, taxes and carry out any other duties

DOWNLOAD THE FULL GUIDE

A Lasting Legacy: Guide to Inheritance and Estate Planning in Ireland

The guide contains all the essential information you need to consider when creating an effective inheritance plan.

Enter your details to download your copy today.